6 Lab: Linear Model Selection and Regularization

This is a modified version of Lab 1: Subset Selection Methods, Lab 2: Ridge Regression and the Lasso, and Lab 3: PCR and PLS Regression labs from chapter 6 of Introduction to Statistical Learning with Application in R. This version uses tidyverse techniques and methods that will allow for scalability and a more efficient data analytic pipeline.

We will need the packages loaded below.

# Load packages

library(tidyverse)

library(modelr)

library(janitor)

library(skimr)

library(leaps) # best subset selection

library(glmnet) # ridge & lasso

library(glmnetUtils) # improves working with glmnet

library(pls) # pcr and plsSince we will be making use of validation set and cross-validation techniques to build and select models we should set our seed to ensure the analyses and procedures being performed are reproducible. Readers will be able to reproduce the lab results if they run all code in sequence from start to finish — cannot run code chucks out of order. Setting the seed should occur towards the top of an analytic script, say directly after loading necessary packages.

# Setting random number generator version

# This is so the code output matches the write-up

RNGversion("3.5")

# Set seed

set.seed(27182) # Used digits from e6.1 Data Setup

We will be using the Hitters dataset from the ISLR library. Take a moment and inspect the codebook — ?ISLR::Hitters. Our goal will be to predict salary from the other available predictors.

hitter_dat <- read_csv("data/Hitters.csv") %>%

clean_names() %>%

rename(c_rbi = crbi) %>%

mutate_at(vars(league, division, new_league), factor)Let’s skim the data to make sure it has been encoded correctly and quickly inspect it for other potential issues such as missing data.

## ── Data Summary ────────────────────────

## Values

## Name Piped data

## Number of rows 322

## Number of columns 21

## _______________________

## Column type frequency:

## character 1

## factor 3

## numeric 17

## ________________________

## Group variables None

##

## ── Variable type: character ────────────────────────────────────────────────────────────────────────

## skim_variable n_missing complete_rate min max empty n_unique whitespace

## 1 name 0 1 7 17 0 322 0

##

## ── Variable type: factor ───────────────────────────────────────────────────────────────────────────

## skim_variable n_missing complete_rate ordered n_unique top_counts

## 1 league 0 1 FALSE 2 A: 175, N: 147

## 2 division 0 1 FALSE 2 W: 165, E: 157

## 3 new_league 0 1 FALSE 2 A: 176, N: 146

##

## ── Variable type: numeric ──────────────────────────────────────────────────────────────────────────

## skim_variable n_missing complete_rate mean sd p0 p25 p50 p75 p100

## 1 at_bat 0 1 381. 153. 16 255. 380. 512 687

## 2 hits 0 1 101. 46.5 1 64 96 137 238

## 3 hm_run 0 1 10.8 8.71 0 4 8 16 40

## 4 runs 0 1 50.9 26.0 0 30.2 48 69 130

## 5 rbi 0 1 48.0 26.2 0 28 44 64.8 121

## 6 walks 0 1 38.7 21.6 0 22 35 53 105

## 7 years 0 1 7.44 4.93 1 4 6 11 24

## 8 c_at_bat 0 1 2649. 2324. 19 817. 1928 3924. 14053

## 9 c_hits 0 1 718. 654. 4 209 508 1059. 4256

## 10 c_hm_run 0 1 69.5 86.3 0 14 37.5 90 548

## 11 c_runs 0 1 359. 334. 1 100. 247 526. 2165

## 12 c_rbi 0 1 330. 333. 0 88.8 220. 426. 1659

## 13 c_walks 0 1 260. 267. 0 67.2 170. 339. 1566

## 14 put_outs 0 1 289. 281. 0 109. 212 325 1378

## 15 assists 0 1 107. 137. 0 7 39.5 166 492

## 16 errors 0 1 8.04 6.37 0 3 6 11 32

## 17 salary 59 0.817 536. 451. 67.5 190 425 750 2460We see there is some missing data/values which are all contained in the response variable salary. There isn’t much we could do here unless we would want to do some research ourselves and see if we can find them somewhere else. We will remove them from our dataset. Note that we could still produce predicted salaries for these players, but we just won’t be able to determine if the predictions are any good.

We will be implementing model selection later in this lab and we have a choice which impacts how we need to handle the dataset. We could opt to use \(C_p\), \(BIC\), or \(R^2_{adj}\) or we could use validation set or cross-validation approaches. Remember that \(C_p\), \(BIC\), or \(R^2_{adj}\) are essentially methods that indirectly estimate test \(MSE\) while validation set or cross-validation approaches provide direct estimates of test \(MSE\). The indirect approaches require many assumptions that may not be tenable and they use the entire dataset. We prefer the direct approaches to estimating test \(MSE\) because they are more flexible and computational limitations are no longer a barrier.

6.2 Subset Selection Methods

## Helper functions

# Get predicted values using regsubset object

predict_regsubset <- function(object, fmla , new_data, model_id)

{

# Not a dataframe? -- handle resample objects/k-folds

if(!is.data.frame(new_data)){

new_data <- as_tibble(new_data)

}

# Get formula

obj_formula <- as.formula(fmla)

# Extract coefficients for desired model

coef_vector <- coef(object, model_id)

# Get appropriate feature matrix for new_data

x_vars <- names(coef_vector)

mod_mat_new <- model.matrix(obj_formula, new_data)[ , x_vars]

# Get predicted values

pred <- as.numeric(mod_mat_new %*% coef_vector)

return(pred)

}

# Calculate test MSE on regsubset objects

test_mse_regsubset <- function(object, fmla , test_data){

# Number of models

num_models <- object %>% summary() %>% pluck("which") %>% dim() %>% .[1]

# Set up storage

test_mse <- rep(NA, num_models)

# observed targets

obs_target <- test_data %>%

as_tibble() %>%

pull(!!as.formula(fmla)[[2]])

# Calculate test MSE for each model class

for(i in 1:num_models){

pred <- predict_regsubset(object, fmla, test_data, model_id = i)

test_mse[i] <- mean((obs_target - pred)^2)

}

# Return the test errors for each model class

tibble(model_index = 1:num_models,

test_mse = test_mse)

}# Best susbset: use 10-fold CV to select optimal number of variables

hitter_bestsubset_cv <- hitter_mod_bldg_dat %>%

crossv_kfold(10, id = "folds") %>%

mutate(fmla = "salary ~ . -name",

model_fits = map2(fmla,

train,

~ regsubsets(as.formula(.x), data = .y, nvmax = 19,)

),

model_fold_mse = pmap(list(model_fits, fmla ,test), test_mse_regsubset)

)

# Forward selection: use 10-fold CV to select optimal number of variables

hitter_fwd_cv <- hitter_mod_bldg_dat %>%

crossv_kfold(10, id = "folds") %>%

mutate(fmla = "salary ~ . -name",

model_fits = map2(fmla,

train,

~ regsubsets(as.formula(.x), data = .y, nvmax = 19, method = "forward")

),

model_fold_mse = pmap(list(model_fits, fmla ,test), test_mse_regsubset)

)

# Backward selection: use 10-fold CV to select optimal number of variables

hitter_back_cv <- hitter_mod_bldg_dat %>%

crossv_kfold(10, id = "folds") %>%

mutate(fmla = "salary ~ . -name",

model_fits = map2(fmla,

train,

~ regsubsets(as.formula(.x), data = .y, nvmax = 19, method = "backward")

),

model_fold_mse = pmap(list(model_fits, fmla ,test), test_mse_regsubset)

)Results for best subset search.

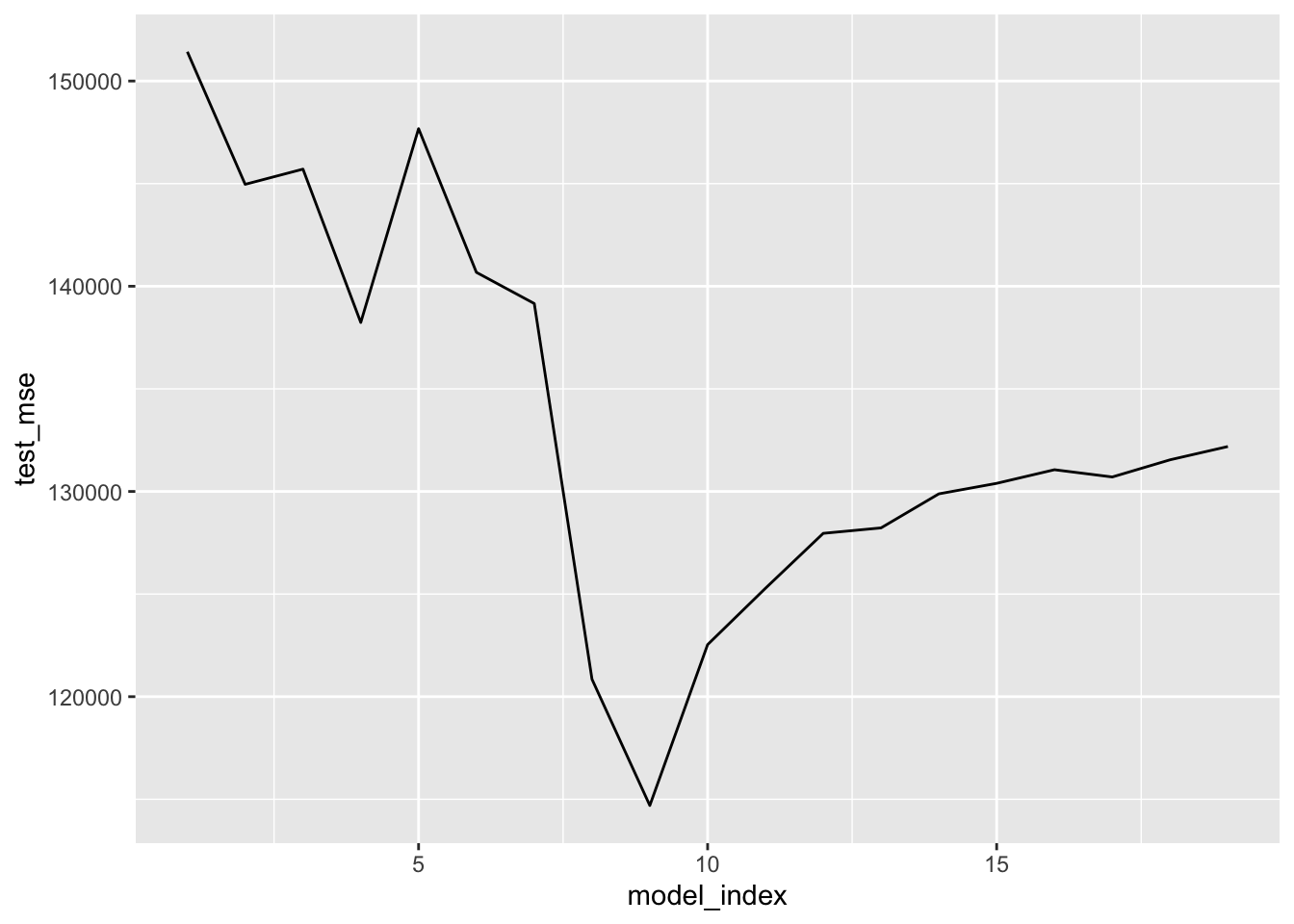

# Plot test MSE (exhaustive search)

hitter_bestsubset_cv %>%

unnest(model_fold_mse) %>%

group_by(model_index) %>%

summarise(test_mse = mean(test_mse)) %>%

ggplot(aes(model_index, test_mse)) +

geom_line()

# Plot test MSE (exhaustive search)

hitter_bestsubset_cv %>%

unnest(model_fold_mse) %>%

group_by(model_index) %>%

summarise(test_mse = mean(test_mse)) %>%

arrange(test_mse)## # A tibble: 19 x 2

## model_index test_mse

## <int> <dbl>

## 1 9 114697.

## 2 8 120848.

## 3 10 122537.

## 4 11 125281.

## 5 12 127959.

## 6 13 128225.

## 7 14 129884.

## 8 15 130396.

## 9 17 130706.

## 10 16 131059.

## 11 18 131543.

## 12 19 132190.

## 13 4 138234.

## 14 7 139159.

## 15 6 140677.

## 16 2 144966.

## 17 3 145706.

## 18 5 147677.

## 19 1 151427.Results for best foward selection search.

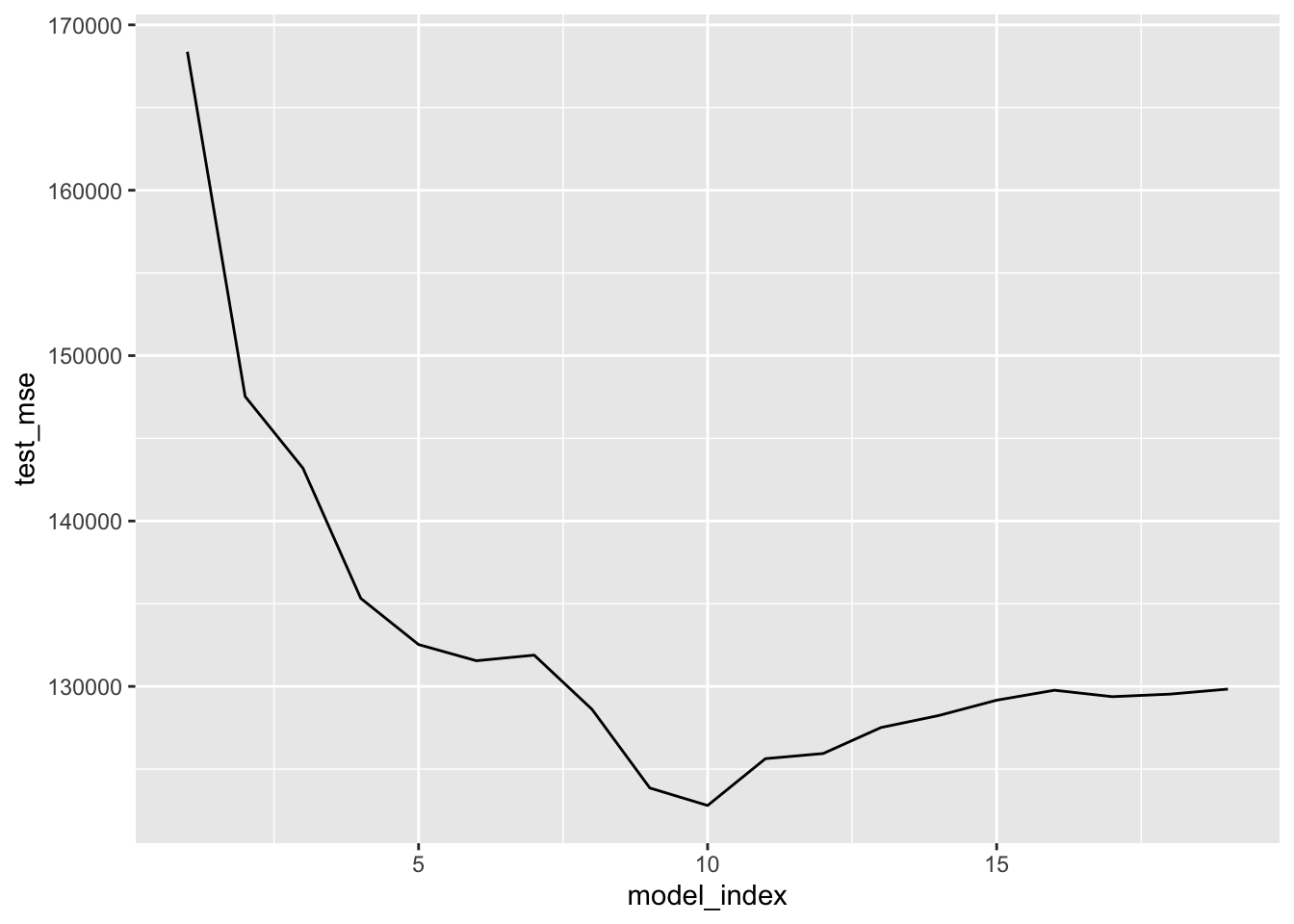

# Plot test MSE (forward search)

hitter_fwd_cv %>%

unnest(model_fold_mse) %>%

group_by(model_index) %>%

summarise(test_mse = mean(test_mse)) %>%

ggplot(aes(model_index, test_mse)) +

geom_line()

# Plot test MSE (forward search)

hitter_fwd_cv %>%

unnest(model_fold_mse) %>%

group_by(model_index) %>%

summarise(test_mse = mean(test_mse)) %>%

arrange(test_mse) ## # A tibble: 19 x 2

## model_index test_mse

## <int> <dbl>

## 1 10 122800.

## 2 9 123859.

## 3 11 125631.

## 4 12 125944.

## 5 13 127514.

## 6 14 128240.

## 7 8 128615.

## 8 15 129167.

## 9 17 129379.

## 10 18 129533.

## 11 16 129768.

## 12 19 129838.

## 13 6 131553.

## 14 7 131891.

## 15 5 132531.

## 16 4 135324.

## 17 3 143196.

## 18 2 147530.

## 19 1 168375.Results for best backward selection search.

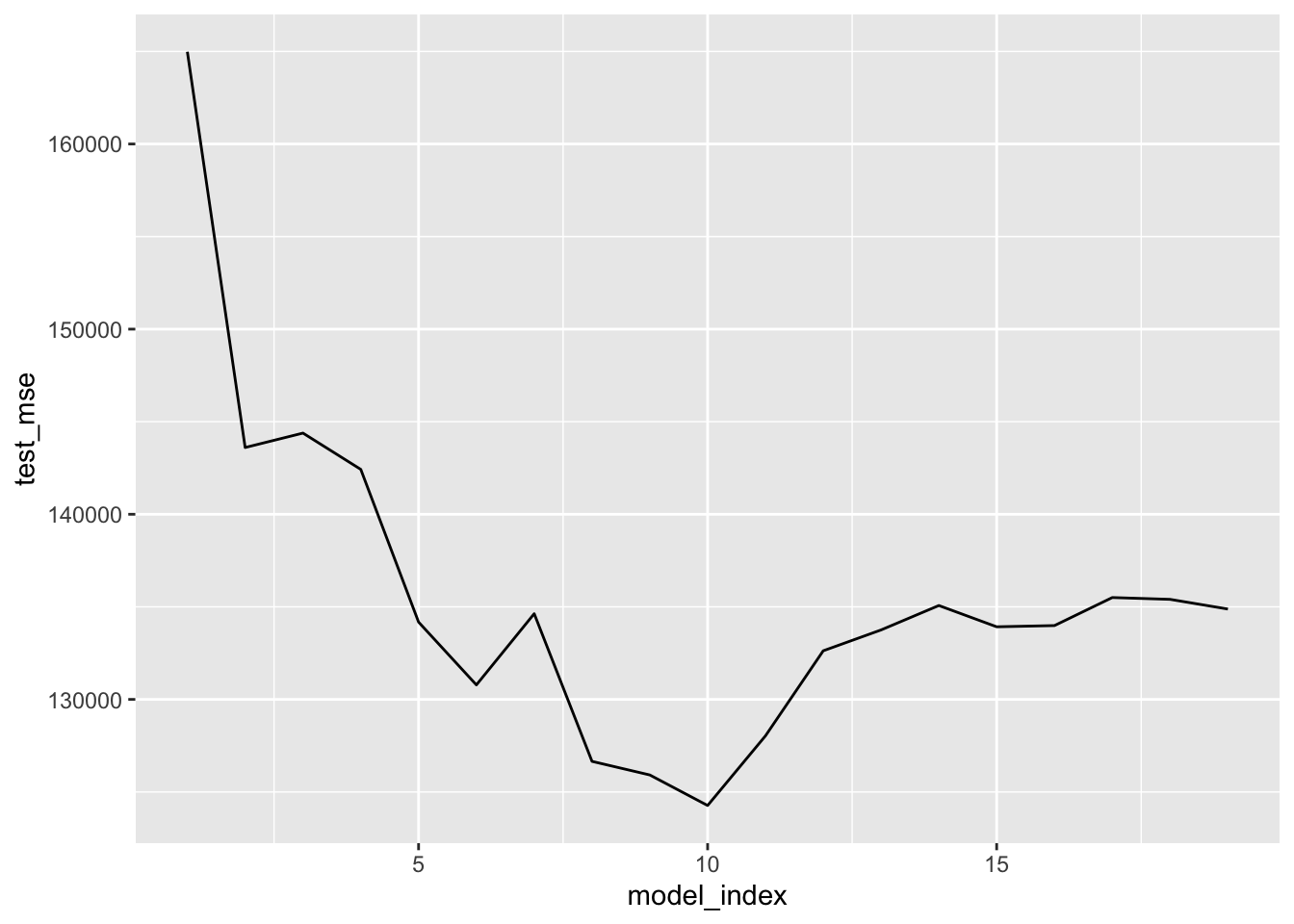

# Plot test MSE (backward search)

hitter_back_cv %>%

unnest(model_fold_mse) %>%

group_by(model_index) %>%

summarise(test_mse = mean(test_mse)) %>%

ggplot(aes(model_index, test_mse)) +

geom_line()

# Table test MSE (backward search)

hitter_back_cv %>%

unnest(model_fold_mse) %>%

group_by(model_index) %>%

summarise(test_mse = mean(test_mse)) %>%

arrange(test_mse) ## # A tibble: 19 x 2

## model_index test_mse

## <int> <dbl>

## 1 10 124270.

## 2 9 125919.

## 3 8 126654.

## 4 11 128029.

## 5 6 130783.

## 6 12 132626.

## 7 13 133752.

## 8 15 133922.

## 9 16 133988.

## 10 5 134176.

## 11 7 134629.

## 12 19 134881.

## 13 14 135071.

## 14 18 135404.

## 15 17 135502.

## 16 4 142425.

## 17 2 143606.

## 18 3 144385.

## 19 1 164982.Results above suggest using a model with 9 predictors — regardless of selection method — would be reasonable. Now implement each selection method on the entirety of hitter_mod_bldg_dat and extract the best model that uses 9 predictors from each. These will be 3 of our candidate models.

hitter_regsubsets <- tibble(train = hitter_mod_bldg_dat %>% list(),

test = hitter_mod_comp_dat %>% list()) %>%

mutate(best_subset = map(train, ~ regsubsets(salary ~ . -name,

data = .x , nvmax = 9)),

fwd_selection = map(train, ~ regsubsets(salary ~ . -name,

data = .x, nvmax = 9,

method = "forward")),

back_selection = map(train, ~ regsubsets(salary ~ . -name,

data = .x, nvmax = 9,

method = "backward"))) %>%

pivot_longer(cols = c(-test, -train), names_to = "method", values_to = "fit")All three of these candidate models have 9 predictors. It is possible that all three methods produce the same model. Let’s take a look at the estimated coefficients for these models.

# Inspect/compare model coefficients

hitter_regsubsets %>%

pluck("fit") %>%

map( ~ coef(.x, id = 9)) %>%

map2(c("best", "fwd", "back"), ~ enframe(.x, value = .y)) %>%

reduce(full_join) %>%

knitr::kable(digits = 3)## Joining, by = "name"

## Joining, by = "name"| name | best | fwd | back |

|---|---|---|---|

| (Intercept) | 139.789 | 141.091 | 133.610 |

| at_bat | -2.093 | -1.556 | -1.741 |

| hits | 6.833 | 5.548 | 6.110 |

| walks | 5.395 | 4.991 | 5.150 |

| c_hm_run | 1.796 | NA | NA |

| c_runs | 0.988 | 1.265 | 1.406 |

| c_walks | -0.903 | -0.824 | -0.935 |

| divisionW | -132.673 | -130.710 | -130.760 |

| put_outs | 0.307 | 0.270 | 0.282 |

| assists | 0.278 | NA | NA |

| c_at_bat | NA | -0.092 | NA |

| c_rbi | NA | 0.692 | 0.683 |

| c_hits | NA | NA | -0.350 |

As the above table demonstrates, the three methods selected three different models that use 9 of the available predictors. There are 7 predictors that all three models have in common. The forward and backward models have 8 predictors in common.

6.3 Ridge Regression & the Lasso

The glmnet package allows users to fit elastic net regressions which includes ridge regression (alpha = 0) and the lasso (alpha =1). Unfortunately the package does not use our familiar formula syntax, y ~ x. It requires the user to encode their data such that the penalized least squares algorithm can be applied. Both lm() and glm() also require the data to be correctly encoded for the least squares algorithm to work but this is done automatically within those functions by using the model.matrix() which takes the inputted formula and appropriately re-encodes the data for the least squares algorithm. glmnet requires the user to use model.matrix() themselves. Wouldn’t it be nice if the glmnet functions did this automatically just like lm() and glm()? Fortunately there is the glmnetUtils package which allows us to keep on using our familiar formula interface with glmnet functions.

The tuning parameter for both ridge regression and the lasso is \(\lambda\), size of the penalty to apply in the least squares algorithm. How do we go about tuning/finding an estimate for the \(\lambda\) parameter? We call upon cross-validation techniques once again. glmnet (glmnetUtils) has a built-in function that will implement cross-validation quickly and efficiently for us. Meaning there is no need for use to use crossv_kfold(). We will be using cv.glmnet() — use ?glmnetUtils::cv.glmnet to access the correct documentation. It is the alpha argument to these functions that determine if we are using ridge regression (alpha = 0) or the lasso (alpha = 1).

Since we are in search of an adequate \(\lambda\) we need to specify a range of values to search. Much like we specified the number of predictors to search over when using regsubset() — started with 1 and went up to 19. The difference here is that \(\lambda\) can be any positive real number (size of penalty to apply). Obviously we cannot use every possible value greater than 0, so we need to setup a grid search. We could go with an automatically selected grid for \(\lambda\) or we can build our own grid. We will demonstrate both.

# lambda grid to search -- use for ridge regression (200 values)

lambda_grid <- 10^seq(-2, 10, length = 200)

# ridge regression: 10-fold cv

ridge_cv <- hitter_mod_bldg_dat %>%

cv.glmnet(formula = salary ~ . - name,

data = .,

alpha = 0,

nfolds = 10,

lambda = lambda_grid

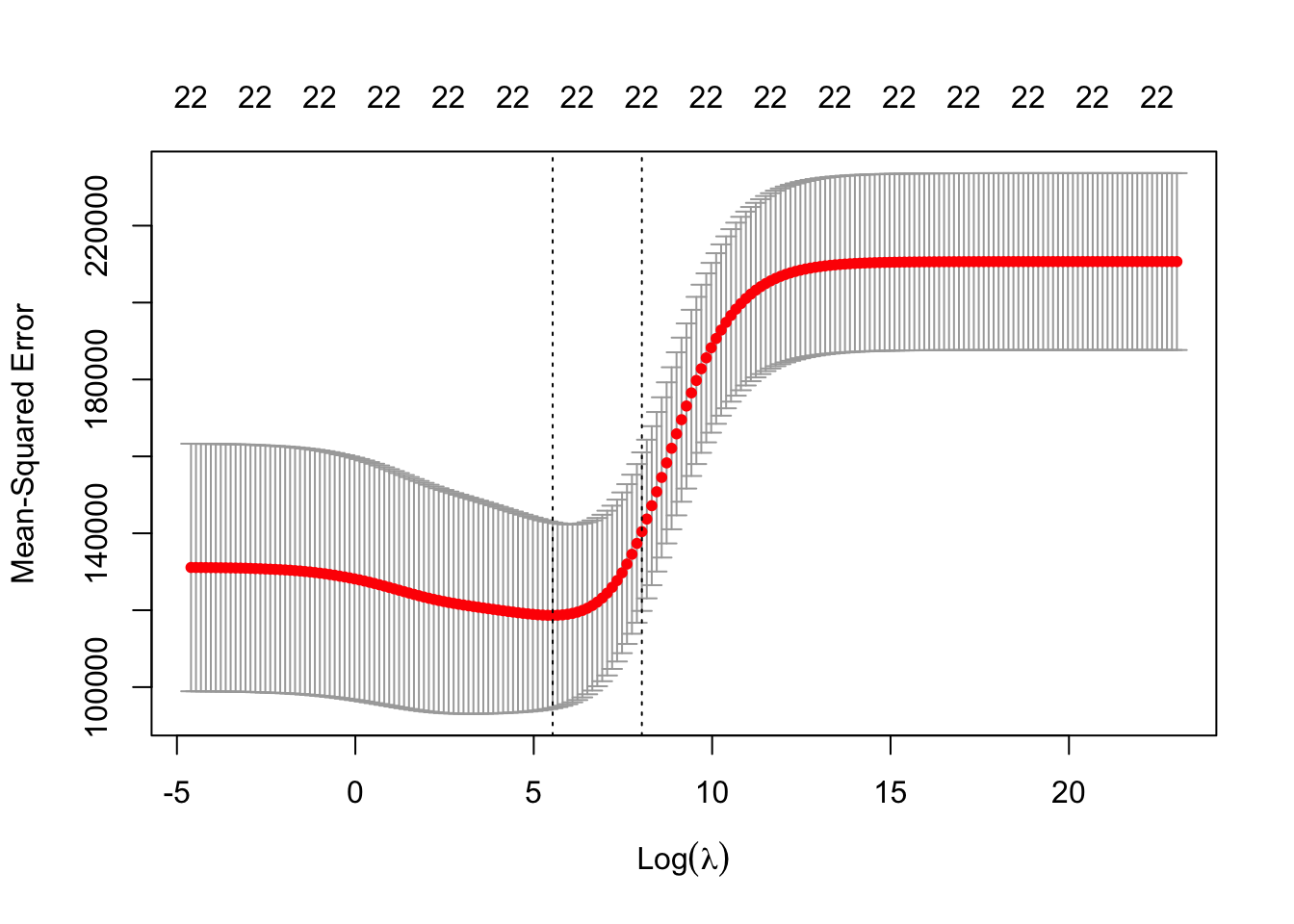

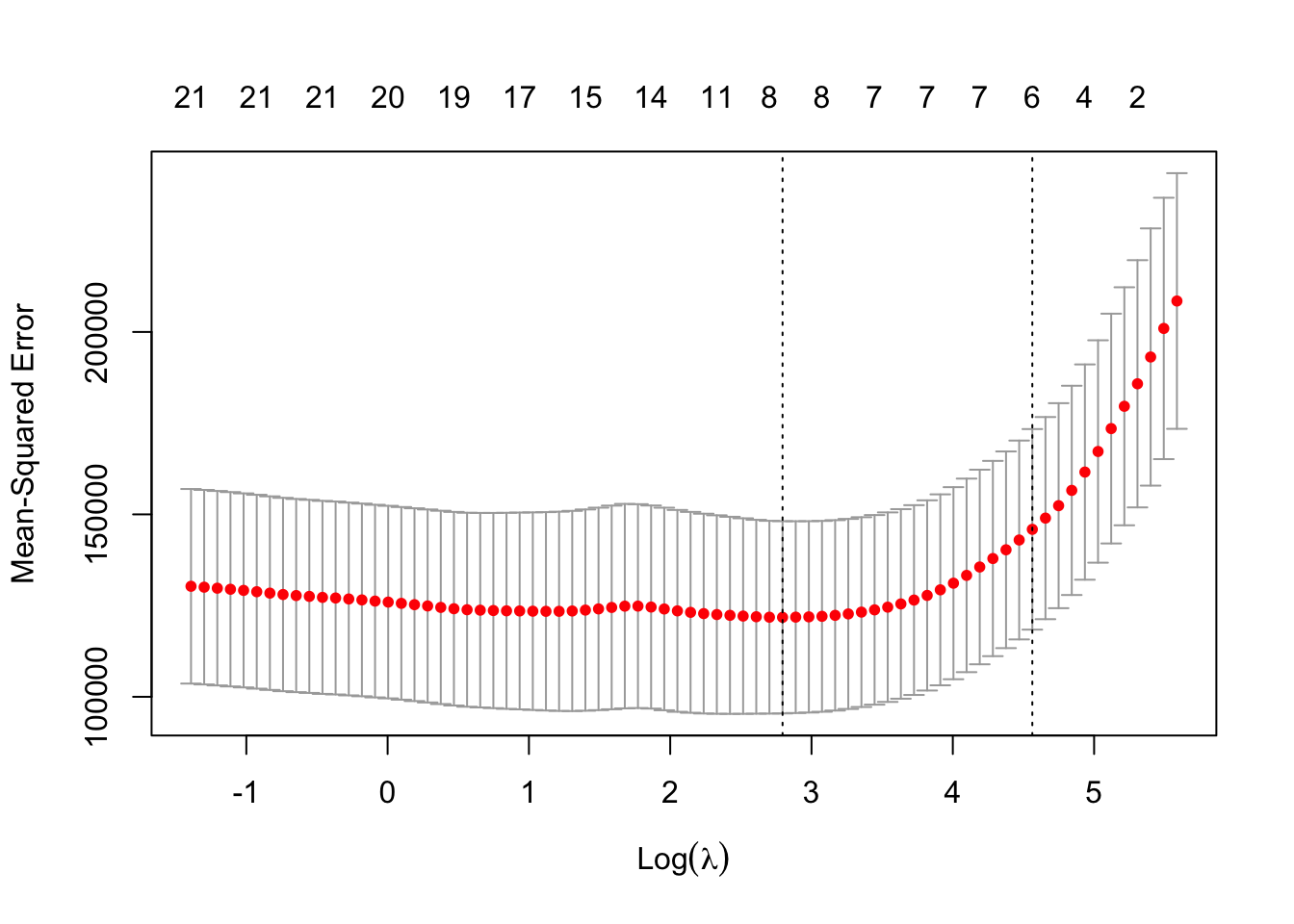

)The following plot displays the 200 estimated test \(MSE\) values using 10 fold cross validation. The plot indicates the minimum \(\lambda\) (left dotted line). The right dotted line corresponds to a \(\lambda\) value that would result in a more regularized model (forcing more or further shrinkage of coefficients towards zero) and is within one standard error of the minimum \(\lambda\) (model’s are not all that different in estimated test \(MSE\)). Why would we desire a more regularized model? A more regularized model will typically shift more of the prediction burden/importance to fewer predictor variables. The top of the plot displays (periodically) the number of predictors in the models and in the case of ridge regression this number is very unlikely to change since it is highly unlikely to force any of the coefficients to be exactly zero.

Strictly speaking the best \(\lambda\) is the one which minimizes the test error. We will extract that value to use for ridge regression. We will also extract the \(\lambda\) that is within one standard error which can help safe guard against over-fitting issues.

# ridge's best lambdas

ridge_lambda_min <- ridge_cv$lambda.min

ridge_lambda_1se <- ridge_cv$lambda.1seLet’s get the best \(\lambda\) values for the lasso. Recall that alpha = 1 now and we will let the function select the search grid for \(\lambda\).

# lasso: 10-fold cv

lasso_cv <- hitter_mod_bldg_dat %>%

cv.glmnet(formula = salary ~ . - name,

data = .,

alpha = 1,

nfolds = 10

)There is an extremely important difference between this plot which is using the lasso and with the plot above which uses ridge regression. The number of predictors is decreasing (top of graph) as \(\lambda\) increases. This is an important distinction between the lasso and ridge regression. Lasso forces coefficients to be zero (i.e. it is performing variable selection). For the lasso a more regularized model will result in a more parsimonious (simpler) model. This is extremely useful when theory indicates that it is likely a handful of variables that are truly related to the response and the others are over-fitting to irreducible error (i.e. won’t be useful for out of sample prediction). For this reason it is fairly standard practice to use lambda.1se as the best \(\lambda\).

# lasso's best lambdas

lasso_lambda_1se <- lasso_cv$lambda.1se

lasso_lambda_min <- lasso_cv$lambda.minNow that we have identified the best \(\lambda\)’s for each method we need to fit them to the entire model building dataset hitter_mod_bldg_dat. These will be our candidate models produced by ridge regression and the lasso. We do this within a tibble framework so that later we are able to calculate each model’s test error (test mse) on hitter_mod_comp_dat. This will allow us to easily compare all of our candidate models against each other in order to pick a final prediction model.

hitter_glmnet <- tibble(train = hitter_mod_bldg_dat %>% list(),

test = hitter_mod_comp_dat %>% list()) %>%

mutate(ridge_min = map(train, ~ glmnet(salary ~ . -name, data = .x,

alpha = 0, lambda = ridge_lambda_min)),

ridge_1se = map(train, ~ glmnet(salary ~ . -name, data = .x,

alpha = 0, lambda = ridge_lambda_1se)),

lasso_min = map(train, ~ glmnet(salary ~ . -name, data = .x,

alpha = 1, lambda = lasso_lambda_min)),

lasso_1se = map(train, ~ glmnet(salary ~ . -name, data = .x,

alpha = 1, lambda = lasso_lambda_1se))) %>%

pivot_longer(cols = c(-test, -train), names_to = "method", values_to = "fit")Let’s take a look at the coefficients for the candidate models produced by ridge regression and the lasso.

# Inspect/compare model coefficients

hitter_glmnet %>%

pluck("fit") %>%

map( ~ coef(.x) %>%

as.matrix() %>%

as.data.frame() %>%

rownames_to_column("name")) %>%

reduce(full_join, by = "name") %>%

mutate_if(is.double, ~ if_else(. == 0, NA_real_, .)) %>%

rename(ridge_min = s0.x,

ridge_1se = s0.y,

lasso_min = s0.x.x,

lasso_1se = s0.y.y) %>%

knitr::kable(digits = 3)| name | ridge_min | ridge_1se | lasso_min | lasso_1se |

|---|---|---|---|---|

| (Intercept) | -18.450 | 232.822 | -73.143 | 221.115 |

| at_bat | 0.085 | 0.088 | NA | NA |

| hits | 0.892 | 0.345 | 2.076 | 1.315 |

| hm_run | 1.199 | 1.247 | NA | NA |

| runs | 0.980 | 0.541 | NA | NA |

| rbi | 0.804 | 0.572 | NA | NA |

| walks | 1.281 | 0.669 | 1.046 | 0.410 |

| years | 1.552 | 2.635 | NA | NA |

| c_at_bat | 0.012 | 0.008 | NA | NA |

| c_hits | 0.060 | 0.028 | NA | NA |

| c_hm_run | 0.615 | 0.243 | 0.970 | 0.464 |

| c_runs | 0.127 | 0.058 | 0.329 | 0.180 |

| c_rbi | 0.139 | 0.062 | 0.154 | 0.206 |

| c_walks | 0.043 | 0.060 | NA | NA |

| leagueA | -12.689 | 0.122 | NA | NA |

| leagueN | 12.693 | -0.122 | NA | NA |

| divisionE | 58.498 | 17.297 | 113.273 | NA |

| divisionW | -58.503 | -17.297 | -2.676 | NA |

| put_outs | 0.195 | 0.048 | 0.247 | 0.026 |

| assists | 0.077 | 0.007 | NA | NA |

| errors | -1.633 | -0.141 | NA | NA |

| new_leagueA | 2.442 | 0.236 | NA | NA |

| new_leagueN | -2.448 | -0.236 | NA | NA |

6.4 PCR & PLS Regression

Will will be using pcr() from the pls library to implement principal component regression. Recall the purpose of PCR is to reduce the dimension of our predictor set. That is we want to find a set of \(m\) principal components (linear combinations of predictors) that we will then use in a linear regression. This is to solve the problem of having too many predictors relative to observations, especially when the number of predictors exceeds that of our observations (\(p > n\)).

Hopefully it is clear that \(m\), the number of principal components, is just a tuning parameter. Meaning we can once again turn to cross-validation techniques to pick the optimal \(m\), optimal in that we want the lowest possible test error. We can set validation = "CV" in pcr() to conduct 10-fold cross-validation by default. Note that you can control the number by specifying, for example, segments = 5 for 5-fold cross-validation.

Before we proceed to tuning the \(m\) parameter there is one more important decision to be made. Do we want to standardize each predictor variable prior to forming the principal components? This is a very important decision because forming principal components is sensitive to scale and standardizing each variable forces them to have the same scale. If we choose to standardize the predictors than we are saying they are all equally important and none should be prioritized over the other due to how it is measured. If not, we are indicating that the scale of the predictor variables is important and should be taken into account when forming principal components. In most cases we will want scale = TRUE because we will have many variables measured on many different scales with no reasonable justification to believe that the scale of the measure should be important. For example a variable such as height does not become more useful when measured in centimeters, then measured in meters.

# pcr: 10-fold cv

pcr_cv <- hitter_mod_bldg_dat %>%

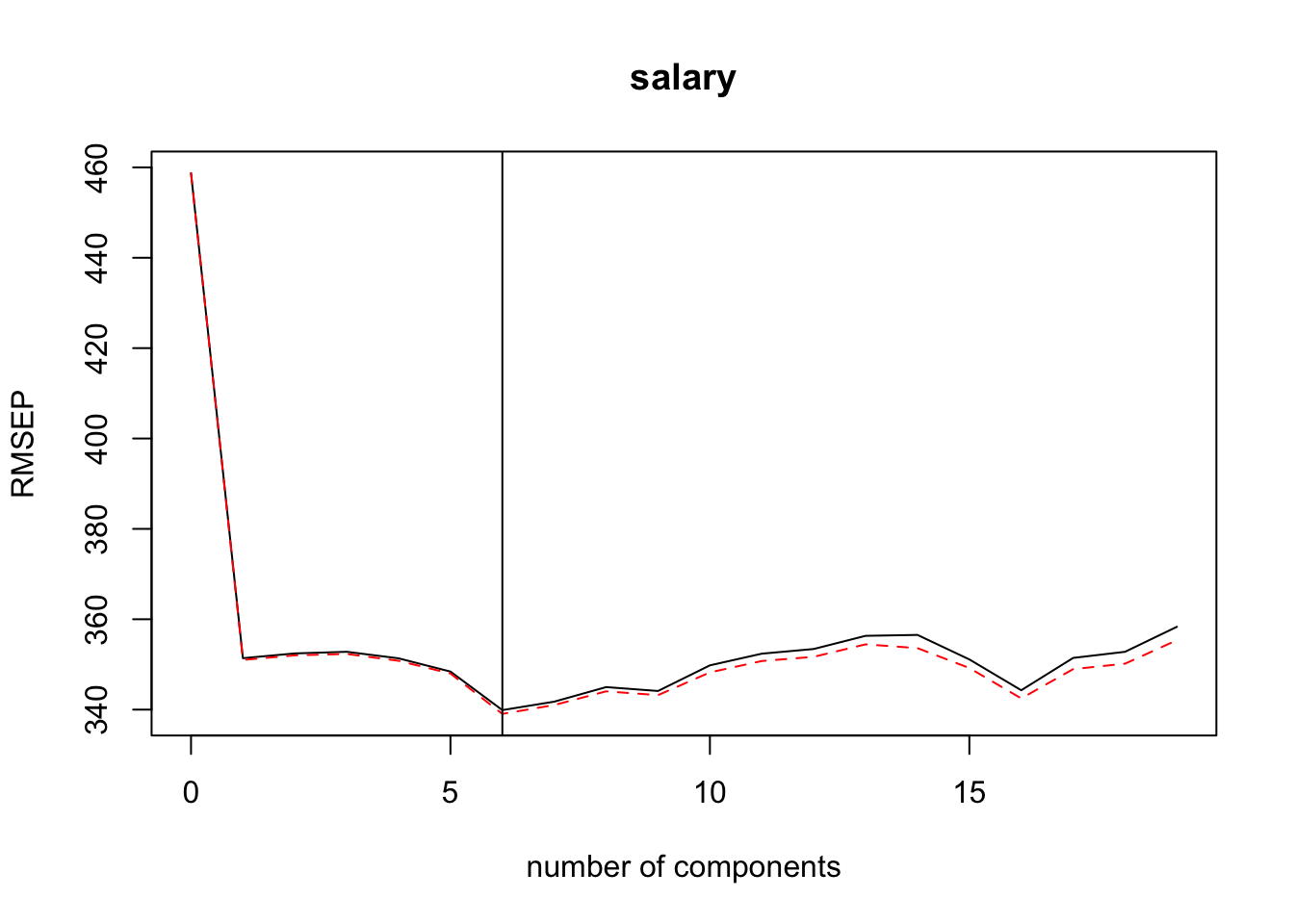

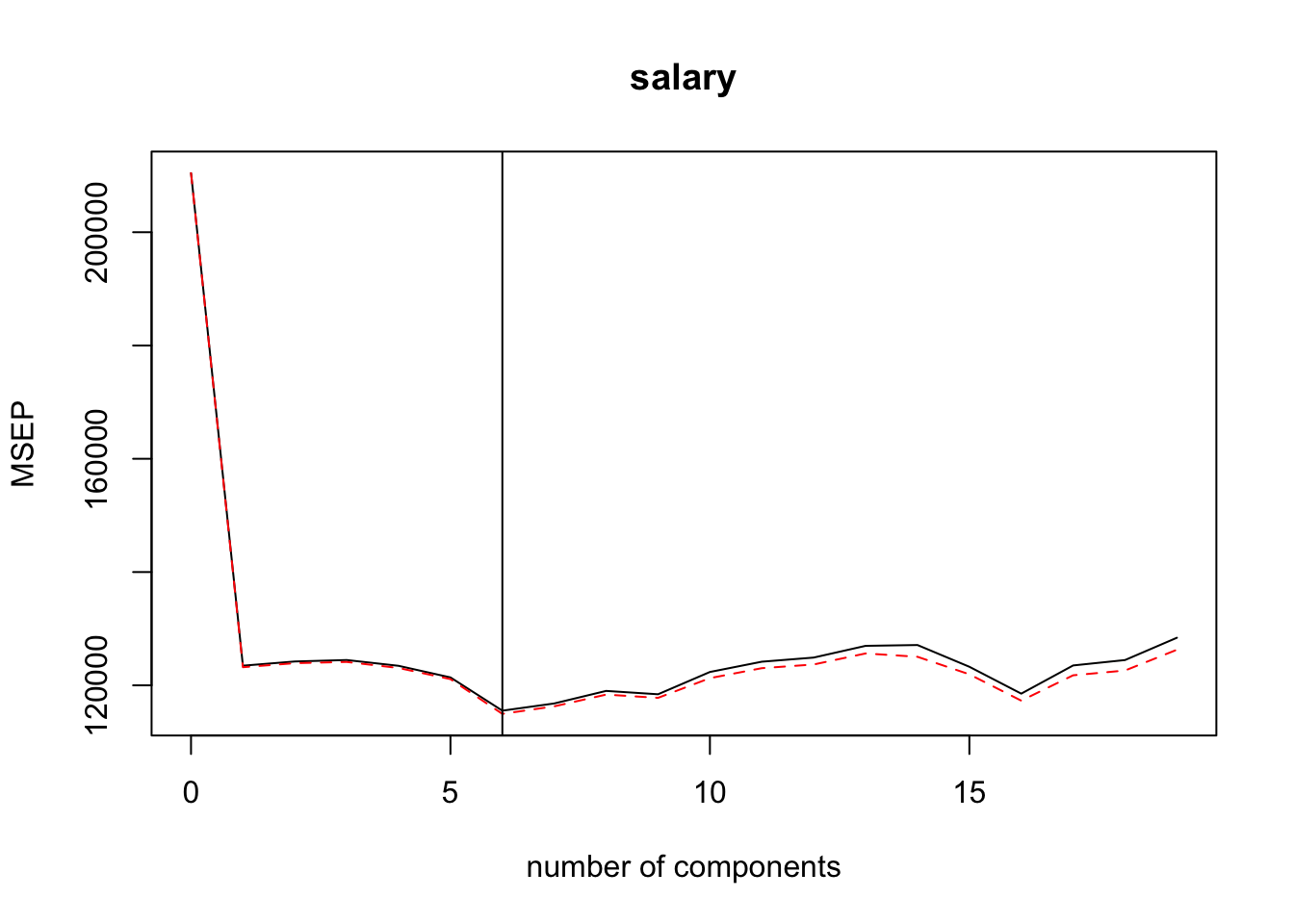

pcr(salary ~ . -name, data = ., scale = TRUE, validation = "CV")We can use validationplot() to find the \(m\) (number of components) that corresponds to the lowest estimated test error (either reported as root mean squared error or mean squared error). The plots below indicate that 6 would be the optimal number of principal components — added a vertical line at 6 to help identify.

# Using mean squared error

validationplot(pcr_cv, val.type="MSEP")

abline(v = 6) # add vertical line at 6

If it becomes too difficult to determine the optimal value using a validationplot() then use summary() to get a table of the values.

## Data: X dimension: 224 19

## Y dimension: 224 1

## Fit method: svdpc

## Number of components considered: 19

##

## VALIDATION: RMSEP

## Cross-validated using 10 random segments.

## (Intercept) 1 comps 2 comps 3 comps 4 comps 5 comps 6 comps

## CV 458.7 351.4 352.4 352.8 351.3 348.4 339.9

## adjCV 458.7 351.0 352.0 352.3 350.8 348.0 339.1

## 7 comps 8 comps 9 comps 10 comps 11 comps 12 comps 13 comps

## CV 341.8 345 344.1 349.8 352.4 353.4 356.3

## adjCV 341.0 344 343.2 348.2 350.8 351.7 354.4

## 14 comps 15 comps 16 comps 17 comps 18 comps 19 comps

## CV 356.5 351.1 344.3 351.4 352.8 358.3

## adjCV 353.6 349.2 342.5 349.0 350.2 355.4

##

## TRAINING: % variance explained

## 1 comps 2 comps 3 comps 4 comps 5 comps 6 comps 7 comps 8 comps

## X 37.57 60.18 71.18 79.31 84.61 88.95 92.34 95.01

## salary 42.30 43.27 43.67 44.55 46.10 48.66 48.66 48.77

## 9 comps 10 comps 11 comps 12 comps 13 comps 14 comps 15 comps

## X 96.31 97.33 98.06 98.73 99.19 99.47 99.75

## salary 49.23 50.39 50.48 50.58 50.59 51.66 51.99

## 16 comps 17 comps 18 comps 19 comps

## X 99.89 99.97 99.99 100.00

## salary 53.62 54.97 55.31 55.38Let’s move on to calculating the optimal \(m\) when using plsr(), partial least squares regression. Note that \(m\) stands for the number of partial least squares directions (much like the number of principal components).

# pls: 10-fold cv

pls_cv <- hitter_mod_bldg_dat %>%

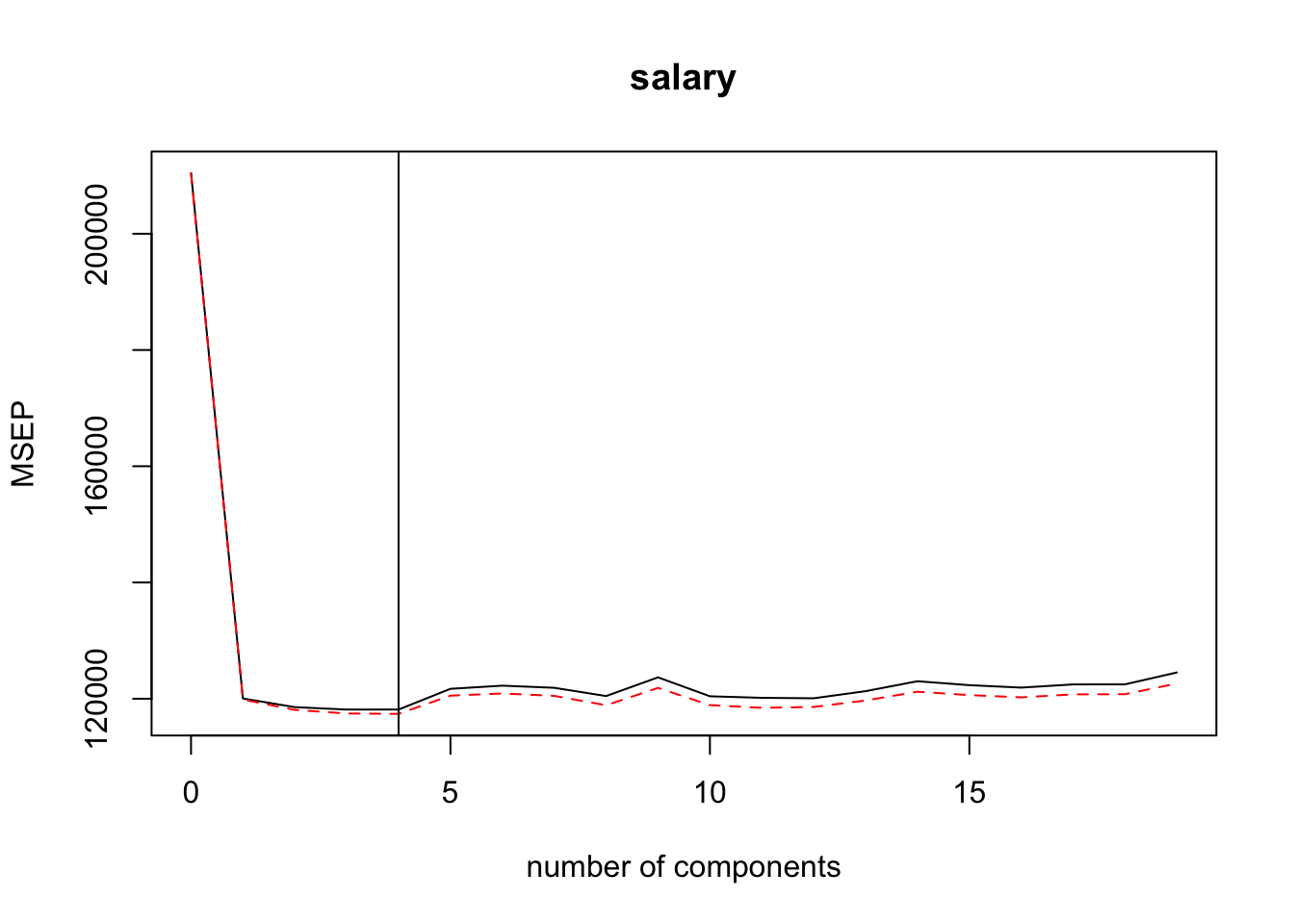

plsr(salary ~ . -name, data = ., scale = TRUE, validation = "CV")Looks like 4 partial least squares directions produce the lowest cross-validation error.

There doesn’t appear to be much difference between using 2, 3 ,or 4 partial least squares directions (see plot above and table below). The fewer directions, the better because the purpose of partial least squares regression is to reduce the dimension of our predictor space. Let’s also plan on proposing a candidate model with 2 parial leat squares directions.

## Data: X dimension: 224 19

## Y dimension: 224 1

## Fit method: kernelpls

## Number of components considered: 19

##

## VALIDATION: RMSEP

## Cross-validated using 10 random segments.

## (Intercept) 1 comps 2 comps 3 comps 4 comps 5 comps 6 comps

## CV 458.7 346.5 344.3 343.7 343.7 348.9 349.6

## adjCV 458.7 346.2 343.6 342.7 342.6 347.2 347.7

## 7 comps 8 comps 9 comps 10 comps 11 comps 12 comps 13 comps

## CV 349.1 347.1 351.7 347.0 346.6 346.5 348.3

## adjCV 347.1 344.8 349.1 344.8 344.1 344.4 346.0

## 14 comps 15 comps 16 comps 17 comps 18 comps 19 comps

## CV 350.7 349.8 349.2 349.9 350.0 352.9

## adjCV 348.1 347.3 346.8 347.5 347.5 350.2

##

## TRAINING: % variance explained

## 1 comps 2 comps 3 comps 4 comps 5 comps 6 comps 7 comps 8 comps

## X 37.35 50.19 65.57 73.78 78.79 84.70 88.71 90.62

## salary 44.80 48.39 49.82 50.67 51.88 52.57 53.18 54.24

## 9 comps 10 comps 11 comps 12 comps 13 comps 14 comps 15 comps

## X 92.81 93.85 94.5 97.24 98.38 98.57 99.15

## salary 54.58 54.85 55.1 55.14 55.19 55.28 55.30

## 16 comps 17 comps 18 comps 19 comps

## X 99.40 99.71 99.97 100.00

## salary 55.34 55.35 55.36 55.38Now that we have identified the best \(m\) for each method we need to fit them to the entire model building dataset hitter_mod_bldg_dat. These will be the candidate models produced by principal component regression and partial least squares regression. We do this within a tibble framework so that later we are able to calculate each model’s test error (test mse) on hitter_mod_comp_dat. This will allow us to easily compare all of our candidate models against each other in order to pick a final prediction model.

hitter_dim_reduct <- tibble(train = hitter_mod_bldg_dat %>% list(),

test = hitter_mod_comp_dat %>% list()) %>%

mutate(pcr_4m = map(train, ~ pcr(salary ~ . -name, data = .x, ncomp = 4)),

pls_2m = map(train, ~ plsr(salary ~ . -name, data = .x, ncomp = 2))) %>%

pivot_longer(cols = c(-test, -train), names_to = "method", values_to = "fit")6.5 Final Model Selection

We will need to calculate the test error for each candidate model produced by the several methods we have previously fit.

# Test error for regsubset fits

regsubset_error <- hitter_regsubsets %>%

mutate(test_mse = map2(fit, test, ~ test_mse_regsubset(.x, salary ~ . -name, .y))) %>%

unnest(test_mse) %>%

filter(model_index == 9) %>%

select(method, test_mse)

# Test error for ridge and lasso fits

glmnet_error <- hitter_glmnet %>%

mutate(pred = map2(fit, test, predict),

test_mse = map2_dbl(test, pred, ~ mean((.x$salary - .y)^2))) %>%

unnest(test_mse) %>%

select(method, test_mse)

# Test error for pcr and plsr fits

dim_reduce_error <- hitter_dim_reduct %>%

mutate(pred = pmap(list(fit, test, c(4,2)), predict),

test_mse = map2_dbl(test, pred, ~ mean((.x$salary - .y)^2))) %>%

unnest(test_mse) %>%

select(method, test_mse)

# Test errors ccombined and organzied

regsubset_error %>%

bind_rows(glmnet_error) %>%

bind_rows(dim_reduce_error) %>%

arrange(test_mse) %>%

knitr::kable(digits = 2)| method | test_mse |

|---|---|

| fwd_selection | 91438.94 |

| back_selection | 96435.69 |

| best_subset | 101786.18 |

| ridge_1se | 115455.82 |

| ridge_min | 116436.23 |

| lasso_1se | 117048.62 |

| lasso_min | 119358.18 |

| pcr_4m | 124611.38 |

| pls_2m | 128228.13 |

Appears that partial least squares regression with 4 directions produces the best model (lowest test mse).